ISA vs SIPP

A complete ISA vs SIPP comparison guide for UK investors

When it comes to saving and investing for the future, UK investors have two powerful tax-efficient tools at their disposal: the Individual Savings Account (ISA) and the Self-Invested Personal Pension (SIPP). Understanding the differences between an ISA and a SIPP can help you make smarter investment decisions and achieve both short-term flexibility and long-term security.

In this blog post, we’ll provide a clear and comprehensive ISA vs SIPP comparison, helping you decide which one fits your financial goals. Whether you’re planning early retirement, looking for the best investment for retirement UK, or simply want to make the most of UK tax-free savings, this guide has you covered.

What is an ISA

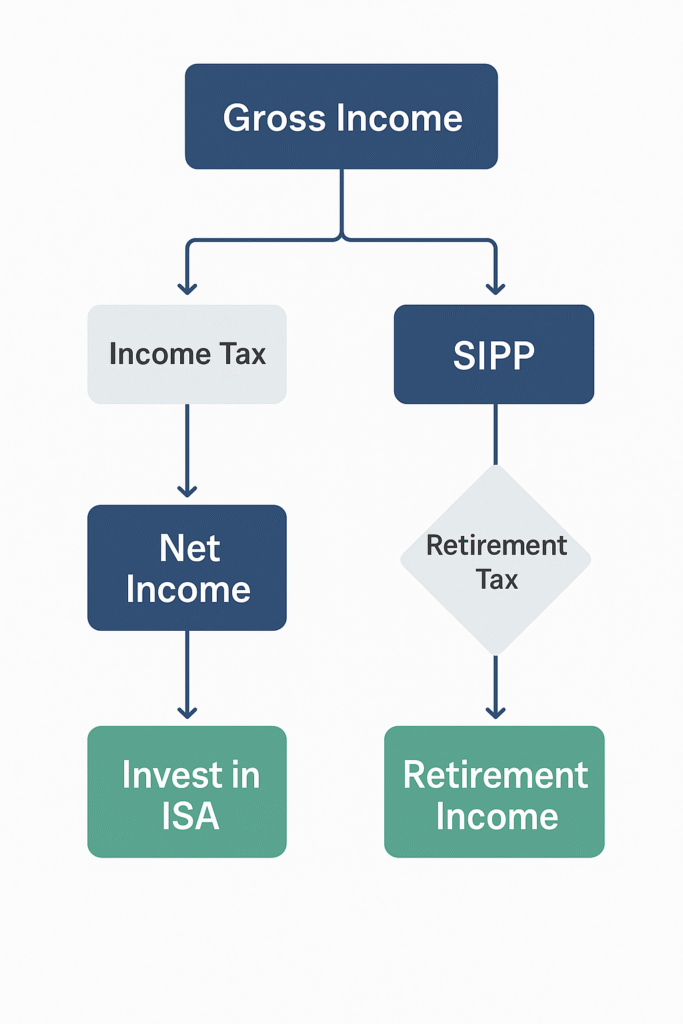

An Individual Savings Account (ISA) is a tax-free savings or investment account available to UK residents. With an ISA, you do not pay income tax or capital gains tax on any returns.

There are several types of ISAs, but the Stocks and Shares ISA is most commonly used for investing. In the 2025/26 tax year, the annual ISA contribution limit is £20,000.

Key features of an ISA:

- Tax-Free Growth: No capital gains or income tax

- Flexibility: Withdraw anytime without penalties

- Annual Limit: £20,000 per tax year

- Eligibility: UK residents aged 18 and above

Using an ISA is one of the most popular methods of UK tax-free savings, offering flexibility and simplicity.

What is a SIPP

A Self-Invested Personal Pension (SIPP) is a type of personal pension that gives you control over your retirement investments. Unlike workplace pensions, a SIPP offers a broad range of investment choices.

The biggest advantage of a SIPP is the tax relief on contributions. For basic-rate taxpayers, the government adds 20% to contributions. Higher-rate taxpayers can claim additional relief through their tax return.

Key Features of a SIPP:

- Tax Relief: 20%-45% depending on income

- Access Age: From age 55 (rising to 57 in 2028)

- Contribution Limit: £60,000 annually or 100% of income (whichever is lower)

- Investment Control: Broad options including shares, funds, bonds, and even commercial property

A SIPP is often considered the best investment for retirement UK due to its powerful tax advantages and long-term growth potential.

ISA vs SIPP Comparison

| Feature | ISA | SIPP |

|---|---|---|

| Tax Relief on Contributions | No | Yes (20-45%) |

| Tax on Withdrawals | No (tax-free) | Yes (75% taxable after 25% tax-free) |

| Access to Funds | Anytime | Age 55+ only |

| Contribution Limits | £20,000/year | Up to £60,000/year |

| Investment Choices | Funds, stocks, ETFs | Funds, stocks, ETFs, commercial property |

| Flexibility | High | Low (due to access age) |

| Inheritance Rules | Subject to inheritance tax | Passed on tax-free if death before 75 |

What's Best to Invest

An ISA is best suited for:

Short to medium-term goals (e.g. house deposit, child’s education)

Emergency fund building

Flexible investing without withdrawal restrictions

The ISA is particularly attractive if you want to invest tax-free in the UK without locking your money away for decades. Since you don’t get upfront tax relief, it's ideal for those who value access over retirement planning.

A SIPP is ideal for:

Long-term retirement savings

High-income earners seeking tax relief

Self-employed individuals with no workplace pension

The self-invested personal pension is especially powerful because of the government top-ups. For every £80 you invest, HMRC adds £20 (for basic-rate taxpayers). Over the long term, this makes a huge difference in your retirement pot.

Yes, and many savvy investors do just that. A smart strategy is to:

Maximise pension contributions (especially if you get employer contributions)

Use your ISA allowance for flexible savings and investing

By doing this, you create both tax-free savings and tax-efficient retirement income.

Tax Implications: A Deeper Look

In short, ISAs give you tax freedom on the way out, while SIPPs give you tax perks on the way in.

What Works Best For Retirement?

When comparing ISA vs SIPP for retirement, SIPPs usually come out ahead for long-term benefits due to tax relief and compound growth. However, they lack flexibility.

ISAs, while flexible and accessible, may not grow as much due to the absence of upfront tax relief. That said, they make a great supplement to a pension and can help bridge early retirement.

This is why many investors prefer to compare ISA and SIPP before deciding how to allocate their savings efficiently.

Decisive Examples

If you're deciding between an ISA or SIPP, the right answer depends on your financial goals

Use ISA

Save for a house deposit in 5 yearsUse SIPP

Supplement workplace pensionUse ISA

Tax-efficient investing with full accessUse SIPP

Retirement planning with tax perksChoose an ISA if you want access, flexibility, and short-to-medium-term investing without tax.

Choose a SIPP if you’re focused on retirement and want to take advantage of government tax relief.

Frequently

Asked Questions

Only in exceptional circumstances such as severe illness or terminal diagnosis.

ISA: Forms part of your estate (subject to inheritance tax)

SIPP: Can be passed on tax-free if you die before age 75

No, they are completely separate wrappers. However, you can invest in similar assets within both.

ISAs are entirely tax-free on the way out. SIPPs are tax-deferred but come with tax relief on the way in.

Pingback: ETF vs Index Funds: Which is Better For UK Investors?